When-the-CRA-Comes-for-Your-Pension

When the CRA Comes for Your Pension: A Canadian’s Story of Hardship and Hope

By Peter Last

For most Canadians, the Canada Pension Plan (CPP) and Old Age Security (OAS) are lifelines. They’re not luxuries—they’re the difference between paying rent and facing eviction, between buying groceries and going hungry.

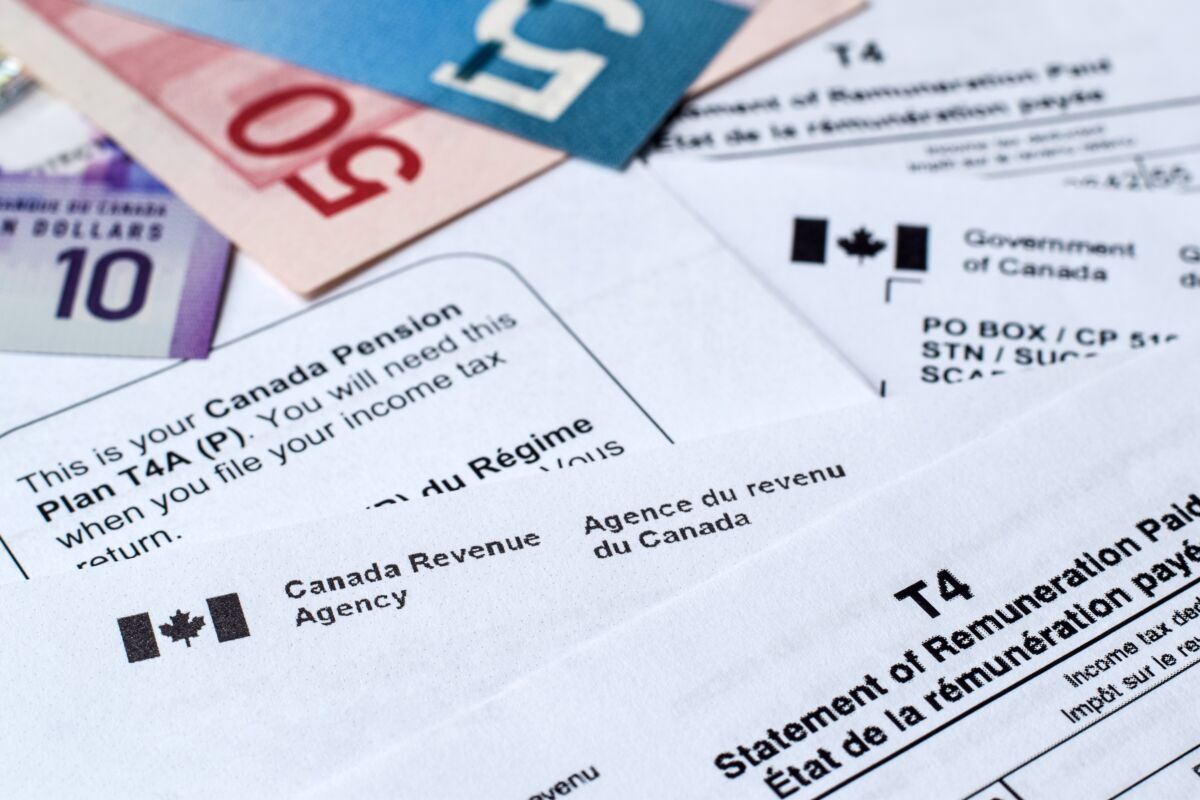

But what many don’t realize is this: the Canada Revenue Agency (CRA) has the power to take those benefits before they ever reach your bank account. They don’t need to ask a judge. They don’t need to prove that you’ll still be able to eat or pay your bills. They simply send a Requirement to Pay under Section 224 of the Income Tax Act—and your money is gone.

I know this because I’m living it.

The CRA claims I owe $247,652.35 in taxes. I have disputed this and requested proof of how they arrived at that number. On July 14, 2025, I sent them a registered letter formally asking for a breakdown of the alleged debt. Canada Post records confirm the CRA received it on July 17, 2025. Yet they verbally told me they hadn’t received my letter—and without providing the requested proof, they still moved forward.

Don’t lose touch with uncensored news! Join our mailing list today.

On July 31, 2025, the CRA issued a Requirement to Pay to my bank and other financial institutions, freezing my accounts. Only later, on August 8, 2025, in a time-stamped envelope, did they mail out these documents to me, which I received on August 11, 2025. The documents they had mailed to me were two weeks after they had already cut me off from my own money. And my initial request on the validation of this amount is still outstanding.

In the meantime, I’ve been doing everything in my power to get my taxes in order. Like many Canadians, I’ve been dealing with significant mental health challenges in the wake of the COVID fallout—struggles that made it hard to focus on anything beyond day-to-day survival. It’s a reminder that one must take care of themselves before they can take care of their obligations to others. Prior to this, I’ve been filing for multiple years, now I find myself gathering every document I can, chasing missing rent receipts and RRSP information from 2021–2024.

I’m repairing my van so I can take on jobs. I’m not hiding from my responsibilities. I’m actively working to resolve this. Now this is on borrowed money from friends. And the irony of it all is, if I’m successful in securing work, I can’t utilize my bank account, and my bank has advised me that if I open an account somewhere else, CRA will find it and do the same thing. This leaves me to question: Is our system designed to force us underground? Is cash really king, or are they just using their overreaching power to control us?

But here’s what Canadians need to understand: if the CRA decides to garnish your income, they can direct Service Canada to send your CPP and OAS straight to them. Or they can order your bank—in my case, the National Bank of Canada—to freeze and remit your RRSP funds. Private creditors can’t touch these benefits without going to court, but the CRA can bypass that entirely.

And here’s the kicker: They can take it all.

Yes, they sometimes leave you with enough to “live on,” but there’s no law requiring them to do so. Unless you successfully plead hardship under the Taxpayer Relief provisions, they could leave you with nothing.

I’ve already filed a hardship claim, but there’s no guarantee it will be respected, after all they have ignored my registered letter. That means my ability to pay rent, keep the lights on, and buy food could be decided in an office far from where I live—by someone named J. Tchuangou #(1231) who’s never met me, never seen my situation, and never walked in my shoes.

This isn’t just about me. It’s about every Canadian who’s worked their whole life, paid into the system, and then finds themselves facing a government agency that can take back what was promised—without a court order, without transparency, and without fair warning.

We need a national conversation about whether that’s right. Because if it can happen to me, it can happen to you.

Explore More...